VA loan pre approval is actually one of the most crucial steps you’ll take as a veteran or active-duty service member looking to buy a home.

If you’re considering using your military benefits to purchase property, you should know that VA Home Loans offer significant advantages. Backed by the Department of Veterans Affairs, these mortgages generally come with no down payment requirements and extremely competitive interest rates. However, navigating the va loan pre approval process can sometimes feel overwhelming.

We’ve helped countless military families through this journey and found that proper preparation makes all the difference. The va home loan pre approval process is essentially a collaborative effort between the VA and private lenders, designed to make homebuying more affordable for those who qualify. Getting pre-approved not only helps you understand your budget but also makes you a more competitive buyer. Specifically, it confirms how much you may be eligible to borrow based on factors like your credit score, income, and debt-to-income ratio.

Our 9 proven tips will guide you through getting pre-approved for your VA loan in 2025, potentially saving you thousands after closing and putting you in the strongest position possible to secure your new home.

Understand VA Loan Preapproval vs. Prequalification

Image Source: Investopedia

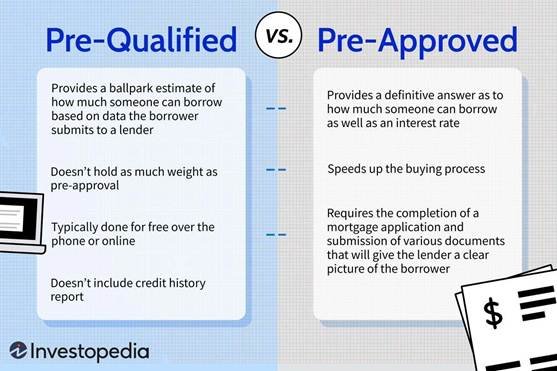

Many veterans confuse the terms prequalification and preapproval when starting their home buying journey. Understanding the difference between these two processes is crucial for a successful VA home purchase.

VA loan preapproval vs. prequalification explained

Prequalification is merely the first step in exploring your VA loan options. During this preliminary process, lenders evaluate basic without verification. It’s a quick conversation where you provide estimates of your income, debts, and assets to get a rough idea of what you might qualify for self-reported financial information[1]. The lender performs a soft credit check that won’t affect your credit score [2].

In contrast, preapproval is a comprehensive financial assessment. Lenders thoroughly review and verify your financial documents, conduct a hard credit check, and confirm your VA loan eligibility [1]. This process takes approximately 1-3 business days to complete, compared to prequalification which typically takes minutes [1].

The key distinction between these processes lies in verification. While prequalification relies on information you provide without documentation, preapproval requires concrete evidence of your financial standing through pay stubs, bank statements, and tax returns [2].

| Feature | Prequalification | Preapproval |

| Based on | Self-reported information | Verified financial documents |

| Credit check | Soft inquiry (no score impact) | Hard inquiry (may affect score) |

| Time to complete | Minutes to hours | 1-3 business days |

| Accuracy | Rough estimate | High-confidence loan amount |

| Documents needed | Minimal | Extensive (income proof, assets, COE) |

Why preapproval is more powerful than prequalification

Preapproval carries significantly more weight with sellers and real estate agents. When you submit an offer with a preapproval letter, you demonstrate that you’re not just window shopping but ready to make a serious purchase [3]. Furthermore, some listing agents and sellers won’t even consider purchase offers from buyers without a preapproval letter [4].

The verification process makes preapproval more credible. Lenders confirm your eligibility, credit, income, and assets upfront, giving you a conditional commitment rather than just an educated guess [3]. Consequently, you’ll receive a preapproval letter stating a specific loan amount you’re qualified to borrow, providing clarity on your true purchasing power [4].

, giving you a reasonable timeframe to find your perfect home Preapproval letters typically remain valid for 60-90 days[2]. During this period, it’s essential to maintain financial stability by avoiding major purchases or changes in employment.

How this impacts your home buying process

Armed with a preapproval letter, you gain several advantages throughout your home buying journey. First, you’ll have a realistic budget based on verified finances rather than estimates, preventing the heartbreak of falling in love with homes beyond your means [4].

Additionally, preapproval strengthens your negotiating position. Sellers recognize that you’ve completed much of the financial verification process, reducing the risk of financing falling through [4]. This can be particularly valuable in competitive markets where multiple offers are common [2].

Moreover, the preapproval process often reveals potential issues that might otherwise surface later. By addressing these challenges early, you can take steps to improve your financial position or adjust your expectations accordingly [2].

Finally, since many underwriting steps are completed during preapproval, you may experience faster closings once you find your home [1]. This efficiency can be a decisive advantage, especially when sellers are comparing multiple offers.

For a successful VA home loan experience, I recommend skipping straight to preapproval if you’re serious about buying. While prequalification provides a helpful starting point for budgeting, preapproval is your golden ticket to making competitive offers in today’s housing market.

Check Your VA Loan Eligibility First

Image Source: MyMilitaryBenefits

Before diving into the VA loan pre approval process, determining your eligibility is the critical first step. Unlike conventional loans, VA home loans require proof of your military service, which is verified through a specific document.

VA loan pre approval requirements

The foundation of your VA loan pre approval begins with meeting the Department of Veterans Affairs’ service requirements. These requirements vary based on your military status and service period:

- Active-duty service members must have served at least 90 continuous days [5]

- Veterans need to have served between 90 consecutive days (wartime) and 181 consecutive days (peacetime), depending on when you served [6]

- National Guard and Reserve members must have either 6 creditable years of service or at least 90 days of active-duty service under Title 32 orders (with at least 30 consecutive days) [6]

- Surviving spouses may qualify if their spouse died during service, is missing in action, being held as a prisoner of war, or died from a service-connected disability [7]

Beyond service eligibility, lenders will examine your credit history, income stability, and debt-to-income ratio during the pre approval process. You must also certify that you’ll use the property as your primary residence, as VA loans cannot be used for vacation or investment properties [6].

How to obtain your Certificate of Eligibility (COE)

The Certificate of Eligibility (COE) is your golden ticket—official proof from the VA that you meet the military service requirements. There are three primary ways to obtain this crucial document:

- Through your lender – This is typically the fastest method. Most VA-approved lenders can access the Web LGY system and generate your COE within seconds in many cases [1]

- Online through the VA’s eBenefits portal – You can request your COE directly through your eBenefits account [6]

- By mail – Complete VA Form 26-1880 (Request for Certificate of Eligibility) and mail it to your regional loan center [1]

The documentation required depends on your military status:

- Veterans need a copy of discharge papers (DD214)

- Active-duty service members need a signed statement of service

- National Guard/Reserve members need specific forms like NGB Form 22 or 23

- Surviving spouses need the veteran’s death certificate and marriage license, plus VA Form 26-1817 [1]

Online and lender-assisted requests often yield immediate results, whereas mail requests typically take 4-6 weeks for processing [5].

Who qualifies for a VA Home Loan

The VA home loan benefit extends to several categories of service members and their families:

- Veterans who were discharged under conditions other than dishonorable and met minimum service requirements

- Active-duty personnel with at least 90 consecutive days of service

- National Guard and Reserve members who completed six years of service or served 90 days on active duty

- Surviving spouses receiving Dependency and Indemnity Compensation or those whose spouse is MIA or POW [7]

Even if you received a discharge other than honorable, you might still qualify under certain exceptions. These include hardship, early out (having served at least 21 months of a 2-year enlistment), convenience of the government, reduction in force, certain medical conditions, or service-connected disabilities [7].

In addition to service eligibility, you must live in the home you’re purchasing. VA loans are approved for single-family homes (up to four units), VA-approved condos, and manufactured homes [6].

Checking your eligibility and obtaining your COE prior to seeking pre approval saves valuable time and prevents potential disappointments. With your COE in hand, you’re ready to move forward confidently in the VA loan pre approval process.

Improve Your Credit Score Before Applying

Image Source: Gustan Cho Associates

Your credit history plays a fundamental role in securing a VA loan pre approval, even though many veterans mistakenly believe perfect credit is required. Understanding how credit impacts your application can make the difference between approval and denial.

Why credit score matters for VA mortgage pre approval

Although the Department of Veterans Affairs itself doesn’t establish a minimum credit score requirement[8], most lenders use your credit history to assess your creditworthiness. Your credit score directly impacts not only your approval odds but also the interest rate you’ll receive [9].

First of all, lenders view your credit score as a reflection of your financial habits. It helps them answer critical questions: Do you repay loans? Are you responsible with credit? Do you consistently make on-time payments? [8] Throughout the underwriting process, your credit history serves as evidence of how you’ve managed financial obligations.

Furthermore, a higher credit score typically qualifies you for better loan terms, potentially saving thousands over the life of your mortgage [10]. This makes credit improvement a worthwhile investment before applying for your VA loan pre approval.

Tips to boost your credit score quickly

Improving your credit score doesn’t happen overnight, yet several strategies can yield results within a few months:

- Pay down credit card balances: Aim to keep your credit utilization ratio (the amount of available credit you’re using) below 30% [7]. This factor accounts for approximately 30% of your FICO score [9].

- Make consistent on-time payments: Payment history is the largest component of your credit score, accounting for 35% of the calculation [9]. Setting up automatic payments can help avoid missed payments.

- Check your credit reports: Request free reports from AnnualCreditReport.com and dispute any errors [6]. This simple step can yield significant improvements if inaccurate negative items are removed.

- Avoid new credit applications: Each application creates a hard inquiry that temporarily lowers your score [7]. Focus on managing existing accounts properly instead.

- Keep old accounts open: The length of your credit history contributes positively to your score [11]. Closing old accounts can unintentionally harm your credit.

For military members facing unique challenges, taking preventive measures before deployment is essential. Setting up automatic payments and placing an “active-duty” alert on your credit reports can protect your score while serving [6].

Minimum credit score most lenders require

Despite the VA not mandating a minimum score, private lenders typically establish their own requirements:

| Loan Type | Minimum Credit Score | Set By |

| VA | 620 (typically) | Lender |

| Conventional | 620 (740 for best terms) | Fannie Mae/Freddie Mac |

| FHA | 500 | HUD |

| USDA | 640 | Lender |

Most VA lenders require a minimum FICO score of 620[8]. Nevertheless, some lenders may accept scores as low as 580 [12], though this often results in higher interest rates to offset the perceived risk.

If your score falls below 620, don’t abandon your homeownership dreams. The best feature of credit is its fluidity—scores change constantly with improved financial habits [8]. Working with lenders who specialize in military borrowers can be particularly helpful, as they understand the unique credit challenges service members face [12].

Lower Your Debt-to-Income Ratio (DTI)

Image Source: Mortgage Calculator

After improving your credit score, focusing on your debt-to-income ratio becomes the next crucial factor for strengthening your VA loan pre approval application. This financial metric often determines whether you can qualify for the loan amount you need.

What is DTI and why it matters for VA loan preapproval

Your debt-to-income ratio fundamentally represents the percentage of your gross monthly income that goes toward paying your debts. For VA loans, lenders examine this ratio to determine if you can comfortably manage additional mortgage payments alongside existing obligations.

While the Department of Veterans Affairs doesn’t set a maximum DTI ratio, they provide guidance that borrowers should ideally have a DTI of 41% or less[13]. Lenders often place additional scrutiny on applications exceeding this threshold [14]. A lower DTI ratio indicates to lenders that you have sufficient income to handle your mortgage payments, making you a less risky borrower.

Unlike conventional loans that consider both front-end and back-end DTI ratios, VA loans primarily focus on the back-end DTI, offering a more comprehensive view of your financial situation [1].

How to calculate your DTI

Calculating your DTI ratio involves a straightforward process:

- Add up all your monthly debt payments (credit cards, car loans, student loans, etc.)

- Divide this total by your gross monthly income (before taxes)

- Multiply by 100 to convert to a percentage

For example, if your monthly debts total $2,300 and your gross monthly income is $5,898, your DTI would be: $2,300 ÷ $5,898 = 0.3899 × 100 = 38.99%[15].

For VA loans, lenders consider major revolving and installment debts from your credit report, plus obligations that may not appear there, such as child care costs [1].

Ways to reduce your DTI before applying

Fortunately, several strategies can help lower your DTI ratio:

- Pay down existing debt: Focus on eliminating smaller debts completely to reduce your monthly obligations [16].

- Increase your income: Consider freelancing, side hustles, or requesting a raise at your current job. Remember that lenders typically require consistent income history [15].

- Add a co-signer: Your legally married spouse or unmarried military members can co-sign on the loan if your DTI is too high [1].

- Consolidate high-interest debts: This can potentially lower your monthly payments and improve your DTI [17].

- Delay major purchases: Postpone buying cars or other financed items until after securing your VA loan [16].

- Use debt repayment strategies: Methods like debt snowball or debt avalanche can systematically reduce your obligations [1].

If your DTI exceeds 41%, don’t lose hope. Lenders may consider compensating factors such as excellent credit history, significant liquid assets, or high residual income [14].

Gather All Required Documents in Advance

Image Source: Griffin Funding

Preparing all necessary paperwork upfront can make your VA loan pre approval process much smoother. Collecting documents before meeting with lenders helps prevent delays and demonstrates you’re a serious borrower.

Documents needed for pre approval for VA home loan

Successful VA loan applications require specific documentation that verifies both your military service and financial situation. The essential documents typically include:

- Certificate of Eligibility (COE) – Proves your VA loan entitlement based on military service [5]

- Government-issued ID – Driver’s license, passport, or military ID card [5]

- Military documentation – DD-214, Statement of Service, or other service verification [18]

- Income verification – Two years of W-2s, recent pay stubs from the past 30 days [18]

- Tax returns – Previous two years of federal tax returns with all schedules [19]

- Bank statements – At least two months of statements from all accounts [19]

- Asset information – Retirement accounts and investment statements [20]

For those with special circumstances, lenders may request additional paperwork including bankruptcy discharge letters, divorce decrees, or VA disability award letters [18].

How to organize your financial paperwork

Firstly, create a digital filing system for easier sharing with lenders. Subsequently, organize your documents into these categories:

- Military/eligibility documentation

- Income verification

- Asset information

- Credit and debt records

- Property information (once you begin house hunting)

Fortunately, most lenders accept digital copies, making organization simpler. Meanwhile, keep original documents safely stored yet accessible throughout your home buying journey.

Common document mistakes to avoid

Many veterans face unnecessary delays due to preventable documentation errors. Primarily, these include:

- Incomplete statements – Bank statements must include all pages, even blank ones, plus your name and account number [18]

- Outdated information – Lenders typically want the most recent 30 days of pay stubs and two months of bank statements [19]

- Unexplained deposits – Be prepared to document the source of any large deposits in your accounts [5]

- Missing signatures – Ensure all required documents have proper signatures [21]

- Starting too late – Understand documentation requirements before making an offer on a home [21]

Obtaining pre-approval should be your initial step when considering buying a home [21]. Henceforth, thorough document preparation increases your chances of a successful application and puts you in a stronger position to make competitive offers.

Choose a VA-Approved Lender with Experience

Image Source: Veterans United

Selecting the right mortgage provider represents a critical decision for your VA loan pre approval journey. Not all lenders have the same level of expertise with veterans’ home loan benefits.

Why working with a VA-approved lender matters

First and foremost, VA loans must come from VA-approved financial institutions[22]. These lenders understand the unique paperwork requirements of military borrowers and can help you obtain your Certificate of Eligibility quickly [23].

Indeed, experienced VA lenders can often access your COE in seconds through the VA’s online portal, saving valuable time [23]. Furthermore, they comprehend VA-specific requirements that conventional mortgage officers might misunderstand or overlook [23].

Expert VA lenders know how to navigate appraisal processes, funding fee exemptions, and military-specific documentation requirements that can make or break your homebuying experience [23].

How to find the right lender for your VA Home Loan

Start by looking for lenders with substantial VA loan experience. Ideally, seek loan officers who close at least five VA purchase loans monthly[8]. Notable options include:

- Banks (like Chase and U.S. Bank) [10]

- Credit unions (particularly those serving military members) [10]

- Online lenders (like Rocket Mortgage) [10]

- VA loan specialists (such as Veterans United) [10]

Naturally, recommendations from fellow veterans who’ve recently used VA loans carry significant weight [24]. Consider the lender’s reputation with real estate agents in your market—those known for closing on time enhance your offer’s competitiveness [6].

Questions to ask your lender

When interviewing potential lenders, consider these essential questions:

“How long have you been offering VA mortgage loans?” [11] Seek lenders with several years of VA loan experience.

“What percentage of your business consists of VA loans?” [6] Higher percentages typically indicate greater expertise.

“What is your average closing timeframe for VA loans?” [6] In competitive markets, 30 days or less is optimal [8].

“Do you charge the full 1% VA origination fee or discount points?” [8] Some lenders charge less than the maximum allowed.

“How does your team communicate throughout the process?” [8] Ensure they have a clear communication plan and secure methods for transmitting sensitive information.

Choosing a knowledgeable VA lender ultimately determines how smoothly your pre approval and homebuying journey progresses.

Get Pre-Approved Before House Hunting

Image Source: MilitaryByOwner

To begin with your home search effectively, getting pre-approved for your VA loan should come before viewing properties. This strategic approach saves time and positions you advantageously in the competitive housing market.

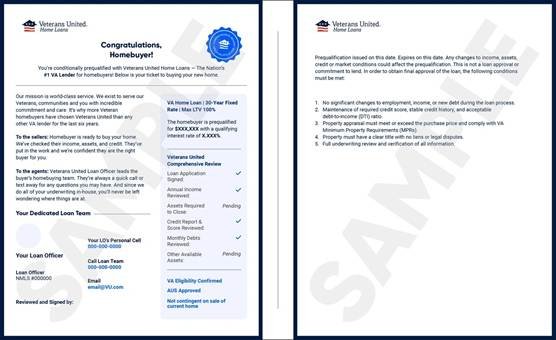

Benefits of having a VA loan pre approval letter

A verified VA loan pre approval letter offers multiple advantages throughout your homebuying journey. Primarily, it provides a clear understanding of your purchasing power, allowing you to focus exclusively on homes within your budget [4]. This prevents the disappointment of falling in love with properties you ultimately cannot afford [25].

Equally important, pre approval streamlines your entire homebuying process by completing many underwriting steps upfront [25]. Your lender performs a thorough review of your credit, income, and assets, giving you confidence that you’re financially prepared to make one of life’s biggest purchases [26].

How preapproval strengthens your offer

In today’s competitive real estate environment, sellers and their agents seek certainty. Undoubtedly, a pre approval letter demonstrates you’re a serious buyer with verified financial backing [27]. In fact, many listing agents and sellers won’t even consider offers without accompanying pre approval documentation [4].

When you present your pre approved VA home loan to sellers, it significantly enhances your negotiating position by:

- Showing you’ve been thoroughly vetted by a lender

- Demonstrating your readiness to proceed quickly

- Reducing the risk of financing falling through

How long VA loan preapproval lasts

VA loan pre approvals typically remain valid for 60 to 90 days[4]. Some lenders may offer shorter timeframes (30 days) or extend validity up to 120 days based on their specific policies [28]. For example, NewCastle Home Loans provides pre approvals valid for four months [26], while Rocket Mortgage offers 90-day pre approvals [27].

Once your pre approval expires, lenders will need to update your financial information and perform another credit check to renew your status [29]. This ensures your financial situation hasn’t changed significantly during your home search.

The ideal timing for obtaining pre approval is one to four months before your planned purchase, giving you adequate time to explore options while maintaining a valid pre approval letter [26].

Understand the VA Funding Fee and Closing Costs

Image Source: AD Mortgage

Beyond getting approved, understanding the costs associated with your VA loan pre approval helps prepare your budget appropriately. The represents a unique expense specific to these government-backed mortgages.VA funding fee

What is the VA funding fee?

The VA funding fee is a one-time payment that helps lower the cost of the VA loan program for U.S. taxpayers [30]. This mandatory fee varies based on several factors:

| Down Payment | First-time Use | Subsequent Use |

| Less than 5% | 2.15% | 3.3% |

| 5% to 9.99% | 1.5% | 1.5% |

| 10% or more | 1.25% | 1.25% |

You can either pay this fee upfront at closing or finance it into your loan amount [30]. Opting to pay upfront saves money on interest over time [31].

Who is ?exempt from the funding fee

Fortunately, certain borrowers qualify for exemption from this fee. You won’t pay the VA funding fee if:

- You receive VA compensation for a service-connected disability

- You’re eligible for disability compensation but receive retirement or active-duty pay instead

- You’re a surviving spouse receiving Dependency and Indemnity Compensation

- You’re a service member with a pre-discharge disability rating

- You’re an active-duty service member awarded the Purple Heart [30]

Should you receive VA disability compensation after closing, you might qualify for a refund if your disability award is retroactive to before your closing date [32].

Other closing costs to prepare for

In addition to the funding fee, anticipate standard closing costs similar to conventional mortgages:

- Loan origination fee (limited to 1% of the loan amount)

- Credit report fees

- VA appraisal fee

- Title insurance and recording fees

- Discount points for lower interest rates [9]

Regarding negotiations, sellers can cover some or all of your closing costs as concessions, but these are limited to 4% of your home’s reasonable value [30].

Use Your Preapproval Letter Strategically

Image Source: Direct Mortgage Loans

Your VA loan pre approval letter serves as a powerful tool in the competitive housing market. Wielding it strategically can significantly strengthen your position when making offers on homes.

How to present your preapproved VA home loan to sellers

Presenting your VA loan pre approval effectively builds seller confidence. Include your lender’s credentials alongside your letter, highlighting their expertise with VA loans to ease seller concerns about loan complexity [12]. A strong pre approval letter demonstrates your financial readiness, making your offer stand out [12]. Furthermore, note your pre approval status in your initial offer as sellers often hesitate working with buyers who haven’t been pre approved [7].

When to update or renew your preapproval

Most VA loan pre approval letters remain valid for 60-90 days[25]. Hence, you’ll need to renew it if your home search extends beyond this timeframe [28]. Primarily, if your pre approval expires while under contract, your lender can typically fast-track the renewal, assuming your finances haven’t changed significantly [28]. Markedly, staying proactive about renewals prevents delays in competitive markets where timing is crucial [28].

How to adjust your letter amount for negotiations

Remarkably, many lenders allow you to tailor the amount shown on your pre approval letter [4]. Consider requesting a letter that matches your offer amount rather than showing your maximum approval [1]. Consequently, if sellers see you qualify for more, they might try negotiating higher [1]. Above all, this strategic approach prevents revealing your full financial capacity during initial negotiations [4].

Comparison Table

| Tip | Main Purpose | Key Requirements | Timeline/Validity | Important Considerations |

| Understand VA Loan Preapproval vs. Prequalification | Differentiate between initial assessment and formal verification | Preapproval: Verified documents, hard credit check; Prequalification: Self-reported info | Prequalification: Minutes; Preapproval: 1-3 business days | Preapproval carries more weight with sellers |

| Check VA Loan Eligibility First | Verify military service qualifications | Active duty: 90 days continuous; Veterans: 90-181 days; National Guard: 6 years or 90 days active | COE processing: Immediate (online) to 4-6 weeks (mail) | Must obtain Certificate of Eligibility (COE) |

| Improve Credit Score Before Applying | Enhance loan approval chances | Typical minimum score: 620 | Credit improvements take several months | Higher scores lead to better interest rates |

| Lower Your Debt-to-Income Ratio (DTI) | Demonstrate ability to manage mortgage payments | Ideal DTI: 41% or less | Not specified | DTI = Monthly debts ÷ Monthly gross income |

| Gather All Required Documents in Advance | Streamline approval process | COE, ID, income verification, tax returns, bank statements | Most recent 30 days of pay stubs; 2 months bank statements | All documents must be complete with signatures |

| Choose VA-Approved Lender with Experience | Ensure expert handling of VA loans | Lender should close at least 5 VA loans monthly | Ideal closing timeframe: 30 days or less | Look for lenders specializing in VA loans |

| Get Pre-Approved Before House Hunting | Determine accurate budget and strengthen offers | Credit, income, and asset verification | 60-90 days validity | Must maintain financial stability during validity period |

| Understand VA Funding Fee and Closing Costs | Plan for upfront expenses | First-time use: 2.15% (0% down); Subsequent use: 3.3% | One-time payment at closing | Some veterans may be exempt |

| Use Your Preapproval Letter Strategically | Strengthen negotiating position | Valid pre-approval letter | 60-90 days before renewal needed | Can request specific amounts for different offers |

Conclusion

Understanding the VA loan pre-approval process thoroughly makes all the difference between a smooth homebuying experience and unnecessary frustration. Military service members deserve to maximize their hard-earned benefits when purchasing a home. Following these nine strategic tips positions you for success in the 2025 housing market.

First and foremost, recognize the critical difference between prequalification and preapproval. Your Certificate of Eligibility serves as the foundation of your VA loan journey, so obtain it early. Meanwhile, work on boosting your credit score and lowering your debt-to-income ratio to secure better loan terms.

Gathering all required documentation before meeting with lenders demonstrates your seriousness and preparedness. Subsequently, choosing a VA-specialized lender significantly improves your chances of approval and ensures expert guidance throughout the process. Getting pre-approved before house hunting both clarifies your budget and strengthens your negotiating position with sellers.

Undoubtedly, understanding all associated costs, particularly the VA funding fee and potential exemptions, helps prevent surprises at closing. Finally, using your pre-approval letter strategically during negotiations can give you a competitive edge in tight markets.

Military families face unique challenges during the homebuying process. However, proper preparation through these proven VA loan pre-approval strategies creates a clear path to homeownership. Your service earned you this valuable benefit – now you have the knowledge to use it effectively. Whether you’re a first-time homebuyer or purchasing your next home, these tips will help you navigate the VA loan process confidently and secure the home you deserve.

Key Takeaways

These proven strategies will help veterans and active-duty service members navigate the VA loan pre-approval process successfully and secure better loan terms in 2025.

• Get pre-approved, not just pre-qualified – pre-approval requires verified documents and carries significantly more weight with sellers in competitive markets.

• Obtain your Certificate of Eligibility (COE) first through your lender, online, or by mail – this proves your military service qualifications for VA loan benefits.

• Aim for a credit score of 620+ and debt-to-income ratio below 41% to qualify for the best interest rates and loan terms available.

• Choose a VA-approved lender who closes at least 5 VA loans monthly and can complete the process within 30 days for competitive advantage.

• Gather all required documents (COE, pay stubs, tax returns, bank statements) in advance to prevent delays and demonstrate serious buyer status.

• Use your pre-approval letter strategically by requesting specific amounts for different offers rather than revealing your maximum qualification to sellers.

Remember that VA loan pre-approvals typically last 60-90 days, giving you a reasonable window to find your perfect home while maintaining your competitive edge in the market.

FAQs

Q1. What is the minimum credit score required for a VA home loan in 2025? While the VA doesn’t set a minimum credit score, most lenders typically require a FICO score between 620 and 670. However, borrowers with lower scores may still qualify with a higher interest rate or larger down payment.

Q2. How long does VA loan pre-approval typically last? VA loan pre-approvals generally remain valid for 60 to 90 days. This gives you a reasonable timeframe to search for a home while maintaining your competitive edge in the market.

Q3. Can sellers cover closing costs on a VA loan? Yes, sellers can contribute to closing costs on a VA loan. However, these seller concessions are limited to 4% of the home’s reasonable value.

Q4. Who is exempt from paying the VA funding fee? Several groups are exempt from the VA funding fee, including veterans receiving VA disability compensation, active-duty service members with a Purple Heart, and surviving spouses receiving Dependency and Indemnity Compensation.

Q5. How does debt-to-income ratio (DTI) affect VA loan approval? While the VA doesn’t set a maximum DTI, most lenders prefer a ratio of 41% or less. A lower DTI demonstrates your ability to manage mortgage payments alongside existing debts, improving your chances of approval and potentially securing better loan terms.