Business loans remain a critical lifeline for entrepreneurs in 2025, with 59% of small businesses seeking new funding during the past 12 months .

Need cash for operating expenses or expansion opportunities? You’re not alone. According to the 2024 Small Business Credit Survey, most businesses (56%) seek financing to cover operational costs, while 46% use funds to expand . The most common types of business loans include term loans, SBA loans, and business lines of credit , with amounts typically ranging from $1,000 to $5 million .

While navigating loan options can be overwhelming, we’ve done the heavy lifting for you. Our experts evaluated 25 lenders to bring you the real costs of different financing options. From term loans with bank interest rates between 6.6% and 11.5% to SBA loans offering up to $5 million in funding (or $5.5 million for select 504 projects) , this guide breaks down everything you need to know about the 12 best business loan types available today.

Term Loans

Image Source: Bankrate

Term loans stand as the foundation of business financing, offering a straightforward approach to capital acquisition. When approved, I receive a single lump sum upfront and repay it through fixed installments over a predetermined period [1].

Term Loans Key Features

Term loans provide structured financing with several distinct characteristics:

- Lump sum funding repaid in fixed installments over a set period [1]

- Available in short-term (less than 1 year), medium-term (1-5 years), or long-term (5+ years) options [1]

- Typically used for specific, one-time expenditures [1]

- Can be secured (requiring collateral) or unsecured [2]

- Often feature fixed interest rates, creating predictable monthly payments [2]

Term Loans Pros and Cons

Pros:

- Predictable repayment schedule helps with budgeting and cash flow management [2]

- Lower interest rates compared to credit cards or cash advances [2]

- Builds business credit when repaid on time [2]

- Extended loan terms (up to 5-7 years) allow for more affordable monthly payments [2]

Cons:

- Many lenders require collateral, putting business assets at risk [2]

- Rigid repayment structure can strain finances during slow periods [2]

- Application process can be lengthy and paperwork-intensive [2]

- Total interest costs can be significant over extended terms [2]

Term Loans Interest Rates

As of 2025, small business bank loan interest rates typically range from 6.6% to 11.5%[3]. For traditional banks specifically, term loan rates average between 7.33% and 7.99% [2]. In contrast, online lenders charge significantly higher rates, ranging from 9% to 75% [2].

Notably, the interest rate structure often depends on loan size:

- Loans under $50,000: Base rate plus 6.5% [2]

- $50,001-$250,000: Base rate plus 6.0% [2]

- $250,001-$350,000: Base rate plus 4.5% [2]

- Over $350,000: Base rate plus 3.0% [2]

Term Loans Best For

Term loans are particularly well-suited for:

- Large equipment purchases or infrastructure upgrades [2]

- Expanding operations, hiring staff, or increasing production capacity [2]

- Business needs around $50,000 for new equipment or vehicles with repayment within a few years [2]

- Planned capital expenditures where preserving cash reserves is important [2]

- Refinancing or consolidating higher-interest debt [2]

- Long-term working capital needs [2]

For instance, a restaurant needing renovations while maintaining cash reserves for seasonal fluctuations would benefit from a term loan’s structured approach [2]. Similarly, construction firms winning new projects requiring immediate equipment purchases find term loans especially valuable [2].

SBA Loans

Image Source: AP News

SBA loans provide government-backed funding through partnerships between the U.S. Small Business Administration and approved lenders. This arrangement creates unique advantages for entrepreneurs seeking capital with favorable terms.

SBA Loans Key Features

SBA loans stand out with several distinctive characteristics:

- , accommodating various business needs Loan amounts ranging from $500 to $5.5 million[2]

- Government guarantees of 50-85% of the loan amount, reducing lender risk [2]

- Longer repayment terms than traditional loans – up to 25 years for real estate [2]

- Lower down payments (sometimes as little as 10% or none for eligible real estate purchases) [3]

- Multiple program options including 7(a), 504, and microloans [2]

Furthermore, these loans offer flexible usage options for almost any business expense, including real estate purchases, equipment acquisition, working capital, debt refinancing, and business acquisitions [2].

SBA Loans Pros and Cons

Pros:

- Capped interest rates make financing more affordable [2]

- Broader eligibility requirements help businesses that might not qualify for traditional loans [2]

- Both small and large loan amounts available to meet diverse needs [2]

- Long-term financing reduces monthly payment burden [2]

- Resource centers provide assistance throughout the loan process [2]

Cons:

- Collateral requirements and personal guarantees for owners with 20%+ stake [3]

- Lengthy approval process (typically 60-90 days) [2]

- Extensive documentation needed for application [2]

- Prepayment penalties on some loans [2]

- Generally unavailable for startups without operating history [2]

SBA Loans Interest Rates

Interest rates for SBA loans combine a base rate plus an additional percentage charged by the lender [2]. As of 2025, depending on loan size maximum fixed interest rates range from 12.5% to 15.5%[2]. Variable rate maximums fall between 10.5% and 14% [2].

The structure follows this pattern:

- Loans under $50,000: Base rate plus 6.5% [2]

- $50,001-$250,000: Base rate plus 6.0% [2]

- $250,001-$350,000: Base rate plus 4.5% [2]

- Over $350,000: Base rate plus 3.0% [2]

SBA Loans Best For

SBA loans are ideally suited for:

- Businesses turned down by traditional lenders but demonstrating growth potential [2]

- Entrepreneurs needing substantial funding with lower down payments [3]

- Companies seeking to purchase commercial real estate with favorable terms [3]

- Business acquisitions or partner buyouts requiring flexible financing [3]

- Established businesses with good credit seeking to refinance high-interest debt [3]

- Companies needing extended repayment periods to maintain healthy cash flow [2]

The 7(a) program remains most popular, with CDC/504 loans better for fixed asset purchases and microloans helping smaller ventures with funding up to $50,000 [4].

Business Lines of Credit

Image Source: The Wall Street Journal

Unlike traditional loans, business lines of credit offer a flexible funding solution with on-demand access to capital. According to the Federal Reserve’s 2024 Small Business Credit Survey, applied for a line of credit for funding, compared to 33% who pursued a business loan 40% of small businesses[1].

Business Lines of Credit Key Features

A business line of credit functions as a revolving source of funds with these key attributes:

- Access to a predetermined credit limit that you can draw from as needed [5]

- Interest only charged on amounts borrowed, not the entire credit limit [5]

- Replenishing availability as you repay, allowing repeated borrowing without reapplication [6]

- Funds accessible through business checking accounts or mobile apps [6]

- Available as secured (requiring collateral) or unsecured options [1]

Business Lines of Credit Pros and Cons

Pros:

- Improves cash flow during seasonal downturns or when facing unexpected expenses [1]

- May be more accessible than traditional loans for startups or those with less-than-perfect credit [1]

- Helps build business credit history with consistent, on-time repayments [1]

- Strengthens lender relationships, potentially leading to better terms in the future [1]

Cons:

- Multiple fees often apply, including origination (up to 5%), maintenance, draw, and annual fees [1]

- Generally shorter repayment terms than term loans, typically 6-24 months with online lenders [1]

- Can lead to a cycle of debt if not managed responsibly [1]

- Typically lower credit limits than traditional term loans [6]

Business Lines of Credit Interest Rates

Business line of credit or higher rates range from 3% to 60%[7]. According to the Small Business Lending Survey, average rates for new business lines of credit in Q4 2024 were between 6.47% to 7.06% for fixed-rate lines and 7.39% to 7.92% for variable-rate lines [7]. Traditional banks offer the most competitive rates, while online lenders charge higher rates with more lenient qualification requirements.

Business Lines of Credit Best For

A business line of credit serves as an ideal solution for:

- Managing cash flow gaps during seasonal fluctuations [8]

- Covering unexpected expenses or emergency situations [9]

- Taking advantage of limited-time opportunities like bulk inventory discounts [8]

- Paying staff or suppliers during periods when receivables are delayed [8]

- Funding short-term projects or marketing initiatives [8]

- Serving as a financial safety net for business operations [6]

Microloans

Image Source: Small Business Administration

Microloans represent a crucial financing avenue for entrepreneurs who struggle to access traditional funding. These small-dollar business loans typically max out at $50,000, with the hovering around $13,000-$15,799 average SBA microloan[2][3].

Microloans Key Features

Microloans function similarly to traditional term loans but with several distinctive characteristics:

- Loan amounts ranging from $500 to $50,000 [2]

- Repayment terms typically between 6 months to 7 years [2]

- Administered by nonprofit community lenders or intermediaries [2]

- Often include business training and educational resources [2]

- Available nationwide through various programs (160 SBA microloan intermediaries serve all 50 states) [2]

Microloans Pros and Cons

Pros:

- Flexible eligibility requirements benefit startups and businesses with limited credit history [2]

- Targeted support for underserved communities including women, minorities, and veterans [2]

- Competitive interest rates compared to alternative financing [2]

- Educational resources and business training frequently included [2]

Cons:

- Limited funding amounts may be insufficient for substantial business needs [2]

- Potentially higher interest rates than traditional bank loans [2]

- Geographical limitations as many microlenders serve only local communities [2]

- Slower funding timeline compared to online loans [2]

Microloans Interest Rates

by provider but remain relatively affordable compared to alternative financing options:Interest rates vary

- SBA microloans: Typically 8% to 13% [2]

- Farm Service Agency: 5% to 5.125% as of 2023 [2]

- Accion Opportunity Fund: 8.49% to 24.99% [2]

- LiftFund: Approximately 10% (varies by qualification) [2]

- Ascendus: 6% to 9.99% [2]

- Justine Petersen: 6% to 20% [2]

- Kiva U.S.: 0% (interest-free) [2][10]

Microloans Best For

Microloans serve as an ideal solution for:

- Startups and newly established businesses with limited operating history [3]

- Entrepreneurs from underserved communities with restricted access to traditional financing [2]

- Small-scale inventory purchases or working capital needs [3]

- Equipment acquisition for micro-entrepreneurs [11]

- Building business credit profiles to qualify for larger loans in the future [10]

- Business owners needing additional support through mentoring and education [10]

Additionally, microloans help fill specific gaps, enabling access to capital for those initially turned away by conventional lenders [10].

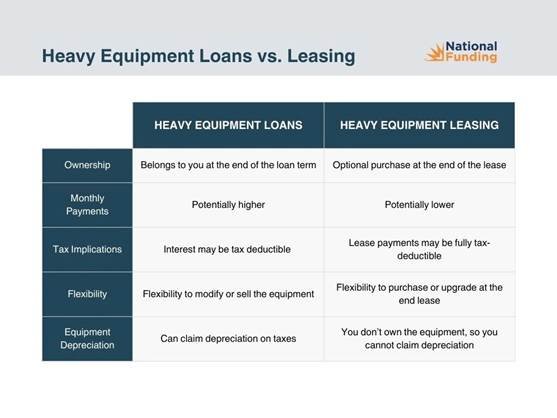

Equipment Loans

Image Source: National Funding

Equipment loans offer a specialized financing solution that enables businesses to purchase necessary machinery without depleting cash reserves. As a secured form of borrowing, these loans use the equipment itself as collateral, often leading to more favorable terms than unsecured alternatives [4].

Equipment Loans Key Features

Equipment loans come with several distinctive attributes:

- Funding amounts typically starting at $5,000 and reaching $500,000+[6]

- Repayment terms generally ranging from 2-7 years, aligned with the equipment’s useful life [5]

- Down payments between 0-30% depending on qualification and lender policies [5]

- Self-collateralizing structure using the purchased equipment as security [4]

- Available through banks, online lenders, and equipment vendors [6]

Equipment Loans Pros and Cons

Pros:

- Quick funding—some lenders offer same-day approval and disbursement [4]

- No additional collateral typically required beyond the equipment itself [4]

- Tax benefits including potential deduction of loan interest and depreciation [12]

- Ownership of the asset after loan repayment, unlike leasing arrangements [4]

- Credit-building opportunity through regular reported payments [4]

Cons:

- Limited financing purpose—funds can only be used for equipment purchases [4]

- Potential high interest rates, especially for borrowers with lower credit scores [4]

- Down payment requirements up to 20% of total equipment cost [4]

- Maintenance costs remain the borrower’s responsibility throughout the loan term [12]

- Risk of the equipment becoming obsolete before the loan is fully repaid [4]

Equipment Loans Interest Rates

Interest rates for equipment financing typically range from 2% to 40%[6]. Agricultural equipment loans from specialized lenders offer rates between 5.99% and 7.45% depending on loan amount and term length [5]. Traditional banks provide the most competitive rates, starting around 5.99% for well-qualified borrowers [5].

Equipment Loans Best For

Equipment loans serve as ideal solutions for:

- Businesses needing to purchase long-lasting equipment with a useful life matching the loan term [13]

- Companies wanting to build equity in business assets rather than leasing [13]

- Organizations seeking tax advantages through depreciation and interest deductions [13]

- Businesses requiring specialized machinery that would strain cash reserves if purchased outright [13]

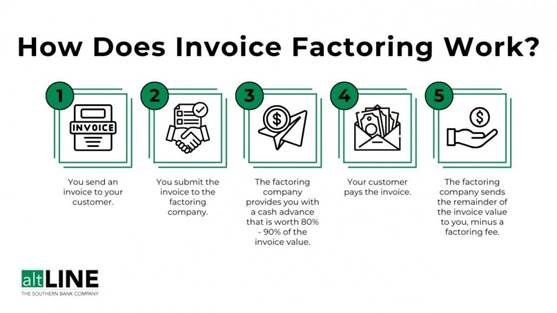

Invoice Factoring

Image Source: altLINE – The Southern Bank Company

Invoice factoring diverges from conventional financing methods by allowing businesses to sell outstanding invoices to a third-party factor at a discount in exchange for immediate cash. Throughout the process, the factoring company takes ownership of invoices and handles collection directly from your customers.

Invoice Factoring Key Features

Invoice factoring operates with these distinctive elements:

- Advances typically range from 70-90% of invoice value paid upfront [1]

- Remaining balance minus fees paid after customer payment collection

- Factoring companies handle customer payment collection

- No debt creation as it’s technically a sale of receivables [14]

- Available as recourse (you’re responsible if customers don’t pay) or non-recourse (factor assumes non-payment risk) [15]

- Quick funding typically within 24-48 hours [16]

Invoice Factoring Pros and Cons

Pros:

- Immediate access to working capital without waiting for slow-paying customers [17]

- Easier qualification process focused on customers’ creditworthiness instead of business credit [1]

- No collateral requirements beyond the invoices themselves [1]

- Can help manage cash flow gaps caused by long payment terms (30-90 days) [17]

- Outsourced collections free up time to focus on core business operations [7]

Cons:

- Higher costs compared to traditional bank loans, with fees ranging from 1-5% monthly[1]

- Loss of direct control over customer relationships as factors handle collections [18]

- Potential hidden fees including wire fees, application fees, and termination fees [19]

- Can be labor-intensive requiring documentation for each invoice submitted [7]

- Factors contact your customers directly, potentially affecting relationships [7]

Invoice Factoring Interest Rates

Invoice factoring rates vary by industry, with monthly fees typically between 1-5% of invoice value [8]. Industry-specific rates include:

- General business: 1.15-4.5% per 30 days with 70-85% advances [8]

- Staffing: 1.15-3.5% per 30 days with 90-92% advances [8]

- Transportation: 1.15-5% per 30 days with 90-96% advances [8]

- Medical: 2.5-4% per 30 days with 60-80% advances [8]

- Construction: 2.5-4.5% per 30 days with 70-80% advances [8]

Invoice Factoring Best For

This financing option works effectively for:

- B2B businesses with slow-paying customers [17]

- Companies needing fast access to working capital [20]

- Businesses unable to qualify for traditional loans or lines of credit [21]

- Startups or companies with limited credit history [20]

- Specific industries including staffing, transportation, manufacturing, wholesale, and professional services [22]

- Seasonal businesses requiring cash flow management between busy periods [23]

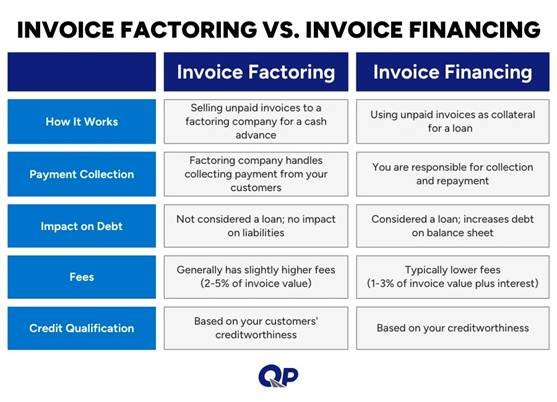

Invoice Financing

Image Source: Quickpay Funding

When facing cash flow gaps from slow-paying customers, invoice financing offers a practical alternative to traditional business loans. This arrangement uses outstanding invoices as collateral while allowing me to maintain control over customer relationships.

Invoice Financing Key Features

Invoice financing operates through several distinctive mechanisms:

- Functions as a cash advance against unpaid customer invoices [9]

- Provides up to 90% of invoice value upfront[9]

- Allows me to retain ownership of invoices and responsibility for collections [9]

- Can be structured as either a loan or line of credit [9]

- Typically funds within 24-48 hours after invoice submission [3]

- Available as disclosed (customer knows) or confidential (customer unaware) [24]

Invoice Financing Pros and Cons

Pros:

- Improves cash flow management during 30-90 day payment waiting periods [3]

- Qualification focuses on customers’ payment history rather than my business credit [9]

- Easier to obtain than traditional loans, especially for startups or businesses with less-than-perfect credit [9]

- Maintains direct control over customer relationships [25]

- Scales with business growth—more invoices mean more available funding [3]

Cons:

- Relatively expensive with fees ranging from 1% to 5% of invoice value monthly[9]

- Total cost depends on how quickly customers pay invoices [9]

- May include additional charges like setup fees ($100-$1,000) and service fees [26]

- Primarily limited to business-to-business companies [9]

- I remain responsible if customers don’t pay [9]

Invoice Financing Interest Rates

Monthly fees typically range from 1-5% of the invoice value [9]. For example, on a $50,000 invoice with 80% advance ($40,000) and 3% monthly fee, I’d pay $1,500 if my customer pays within 30 days [27]. This calculates to an effective APR of approximately 45% [27].

Invoice Financing Best For

Invoice financing works optimally for:

- B2B companies experiencing cash flow issues due to unpaid invoices [27]

- Businesses wanting to maintain control over their accounts receivable process [27]

- Companies with strong customer relationships and efficient collection processes [27]

- Seasonal operations needing to smooth out cash flow fluctuations [28]

- Organizations requiring quick access to working capital without long-term debt [3]

Merchant Cash Advances

Image Source: Clarify Capital

Merchant cash advances stand apart from conventional financing options as they’re technically not loans but purchases of future sales. These financial products have gained popularity, with in 2022 10% of small businesses seeking MCAs[29].

Merchant Cash Advances Key Features

Merchant cash advances operate through a distinct structure:

- Lump sum funding in exchange for a percentage of future credit/debit card sales [11]

- Repayment occurs daily or weekly through automatic deductions [30]

- Funding typically arrives within 24-48 hours after approval [2]

- No set repayment period—payments fluctuate with sales volume [11]

- Factor rates (typically 1.1 to 1.5) determine total repayment amount [11]

- Requires established daily credit card transactions with at least four months of credit sales [11]

Merchant Cash Advances Pros and Cons

Pros:

- Almost immediate access to cash—often funded within one day [11]

- Easy qualification with minimal documentation requirements [11]

- No collateral necessary beyond future sales [29]

- Flexible payments that adjust based on sales volume [29]

Cons:

- Extremely high costs— APRs can reach triple digits (up to 200%)[11]

- Daily or weekly payment frequency can strain cash flow [11]

- Largely unregulated industry with potential for predatory practices [29]

- Creates risk of debt cycles where businesses need new advances to pay existing ones [11]

Merchant Cash Advances Interest Rates

Factor rates typically range from 1.1 to 1.5 [11]. With a factor rate of 1.5 on a $40,000 advance, you’ll repay $60,000 total ($40,000 + $20,000 in fees) [11]. This structure creates fixed costs regardless of how quickly you repay [10]. Most MCA providers don’t report to credit bureaus, so these advances don’t build business credit [29].

Merchant Cash Advances Best For

MCAs work best for:

- Businesses unable to qualify for traditional financing [11]

- Companies needing immediate capital access [30]

- Established businesses with consistent credit card sales (typically $2,500-$5,000 monthly) [11]

- Merchants requiring funding for short-term needs [31]

- Restaurant, retail, and service businesses with high card transaction volumes [32]

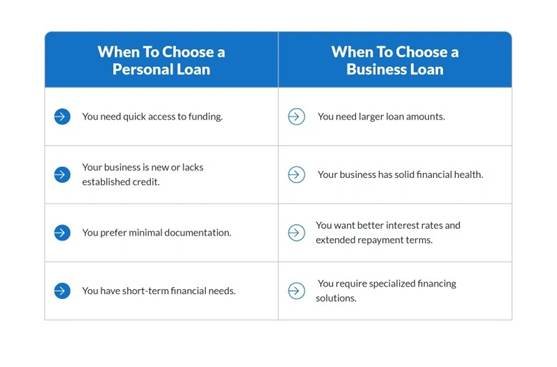

Personal Loans for Business

Image Source: Bankrate

Personal loans emerge as an alternative financing route for entrepreneurs who lack access to traditional business funding. Although not designed specifically for commercial purposes, many lenders allow their personal loans to be used for business expenses.

Personal Loans for Business Key Features

Personal loans for business financing offer distinct characteristics:

- Loan amounts typically ranging from $1,000 to $100,000[33]

- Repayment terms between 2-7 years with fixed monthly payments [34]

- Approval based on personal credit score and income rather than business financials [34]

- Typically unsecured, requiring no collateral [35]

- Quick funding often within 24-48 hours after approval [36]

- Funds can be used flexibly for various business purposes [33]

Personal Loans for Business Pros and Cons

Pros:

- Easier qualification process focused on personal finances [34]

- Faster approval and funding compared to business loans [35]

- No collateral requirements with unsecured options [35]

- Ideal for startups without established business credit [37]

Cons:

- Higher interest rates compared to traditional business loans [34]

- Lower borrowing limits typically capped at $100,000 [34]

- Personal liability for debt regardless of business performance [38]

- No opportunity to build business credit history [37]

Personal Loans for Business Interest Rates

Interest rates for personal loans used for business purposes typically range from 6.5% to 36% [34]. This contrasts with business loan rates that average between 7.33% and 7.99% [34]. Your personal credit score heavily influences the rate you’ll receive [39].

Personal Loans for Business Best For

This financing option works effectively for:

- New startups without sufficient operating history for business loans [36]

- Entrepreneurs with strong personal credit but limited business credentials [35]

- Small-scale funding needs under $50,000 [35]

- Businesses requiring quick capital access without extensive documentation [33]

- Ventures considered higher-risk by traditional lenders [36]

Business Credit Cards

Image Source: BMO

Business credit cards function as revolving lines of credit that offer unique advantages for entrepreneurs managing day-to-day expenses. As a financial tool specifically designed for business owners, these cards provide a convenient alternative to traditional business loans for certain financing needs.

Business Credit Cards Key Features

Business credit cards operate as a revolving credit line allowing purchases within a specified limit [40]. Once approved, I can make repeated purchases without reapplying as long as I stay below my credit limit [12]. These cards typically offer higher spending limits than personal cards [41], free employee cards [42], and dedicated expense tracking tools that automatically categorize business spending [41].

Business Credit Cards Pros and Cons

Pros:

- Separates business and personal finances, simplifying tax preparation [41]

- Builds business credit history with responsible use [4]

- Earns rewards on business-specific categories like office supplies and travel [40]

- Provides purchase protection and extended warranties [5]

- Offers flexibility with access to funds as needed [4]

Cons:

- High variable interest rates ranging from 18% to 36% [4]

- Potential negative impact on personal credit if payments are missed [12]

- Fewer federal protections compared to consumer credit cards [41]

- Possible annual fees and other charges [12]

Business Credit Cards Interest Rates

Interest rates typically range from 13% to 20% based on creditworthiness [43], with most cards offering a variable APR between 17.49% and 27.49% [5]. Premium business cards with extensive rewards programs frequently charge higher rates [44]. Many cards offer introductory 0% APR periods lasting 7-9 months [5].

Business Credit Cards Best For

These cards work exceptionally well for paying everyday business expenses while earning rewards [4]. They’re also ideal for startups establishing financial history [41], businesses needing to separate personal and business finances [5], and companies wanting to monitor employee spending through controlled employee cards [41].

Commercial Real Estate Loans

Image Source: Corporate Finance Institute

Commercial property loans enable business owners to purchase, build, or refinance real estate for business use. These specialized financing options differ substantially from residential mortgages in terms, conditions, and qualification requirements.

Commercial Real Estate Loans Key Features

Commercial real estate loans offer distinct characteristics:

- Loan amounts from $25,000 to several million dollars

- Terms typically 5-10 years with balloon payments or up to 25 years for some options

- Down payments ranging from 20-40% of property value

- Qualification requires minimum 2 years in business and $250,000+ annual revenue

- Available for various property types including office, retail, industrial, and multifamily

Commercial Real Estate Loans Pros and Cons

Pros:

- Lower interest rates compared to unsecured business loans

- Potential property value appreciation over time

- Possibility to generate additional income by leasing extra space

- Building equity with each payment

- Flexible options if business needs to relocate or close

Cons:

- Substantial upfront costs including 20-40% down payment [45]

- Complete responsibility for property maintenance and repairs

- Vulnerability to market fluctuations affecting property value

- Sensitivity to interest rate changes with variable-rate options

- Less liquidity than residential properties during sales [45]

Commercial Real Estate Loans Interest Rates

Interest rates vary by loan type and borrower qualifications:

- Conventional commercial loans: 6% to 10% [6]

- SBA 504 loans: 5% to 7% [6]

- Bridge loans: 7% to 14% [6]

- Construction loans: 8% to 13% [6]

Commercial Real Estate Loans Best For

These loans work optimally for:

- Businesses wanting to eliminate leasing uncertainties through ownership

- Companies seeking to build equity while securing operational space

- Organizations looking to generate additional revenue through partial property leasing

- Established businesses ready to invest in permanent locations

Startup Business Loans

Image Source: Clarify Capital

Financing a newly established venture presents unique challenges, as most conventional lenders require years of business history. Startup business loans bridge this gap, offering capital solutions specifically designed for entrepreneurs with limited operating experience.

Startup Business Loans Key Features

Startup loans typically provide amounts ranging from $500 to $5 million [46], with eligibility requirements less stringent than traditional financing. Many lenders accept businesses with just six months of operation [46], though some may require evidence of revenue or strong personal credit. Application processes typically involve submitting business plans, financial projections, and personal financial statements [47].

Startup Business Loans Pros and Cons

Pros:

- Fast access to capital helps launch operations quickly [13]

- Builds business credit with timely payments [13]

- Offers tax advantages not available with personal funding [13]

- Protects personal assets when structured properly [13]

Cons:

- Risk of default if business doesn’t generate expected revenue [13]

- Higher interest rates compared to established business loans [46]

- Often requires personal guarantees [13]

- Can be costly with various fees and charges [13]

Startup Business Loans Interest Rates

Interest rates vary considerably based on lender type and business qualifications. According to recent data, rates typically range from 7% to 99% [17]. Those with excellent credit may secure rates as low as 7-8% [17], whereas online lenders often charge significantly more.

Startup Business Loans Best For

These loans serve ideally for entrepreneurs with strong personal credit [13], solid revenue projections [13], and clear plans for fund utilization [13]. Moreover, they benefit businesses needing immediate capital access rather than waiting for crowdfunding or grants [13].

Comparison Table

| Loan Type | Typical Loan Amounts | Interest Rate Range | Key Features | Best Suited For | Major Drawbacks |

| Term Loans | $1,000 – $5M | 6.6% – 11.5% (banks)9% – 75% (online) | Fixed installments, set repayment period | Large equipment purchases, expansion, infrastructure upgrades | Collateral often required, rigid repayment structure |

| SBA Loans | $500 – $5.5M | 12.5% – 15.5% (fixed)10.5% – 14% (variable) | Government-backed, longer repayment terms | Businesses turned down by traditional lenders, real estate purchases | Lengthy approval process (60-90 days), extensive documentation |

| Business Lines of Credit | Not specified | 3% – 60% | Revolving credit, pay interest only on used amount | Managing cash flow gaps, seasonal fluctuations | Multiple fees, shorter repayment terms |

| Microloans | $500 – $50,000 | 8% – 13% (SBA)0% – 24.99% (various) | Include business training, administered by nonprofits | Startups, underserved communities | Limited funding amounts, geographical limitations |

| Equipment Loans | $5,000 – $500,000+ | 2% – 40% | Self-collateralizing, equipment serves as security | Businesses needing specific machinery/equipment | Limited to equipment purchases, potential obsolescence |

| Invoice Factoring | 70-90% of invoice value | 1% – 5% monthly | Quick funding (24-48 hours), factor handles collections | B2B businesses with slow-paying customers | Higher costs, loss of customer relationship control |

| Invoice Financing | Up to 90% of invoice value | 1% – 5% monthly | Retain control of collections, quick funding | B2B companies with unpaid invoices | Expensive, limited to B2B companies |

| Merchant Cash Advances | Not specified | Factor rates 1.1 – 1.5 (up to 200% APR) | Daily/weekly repayment based on sales | Businesses with consistent credit card sales | Extremely high costs, frequent payments |

| Personal Loans for Business | $1,000 – $100,000 | 6.5% – 36% | Based on personal credit, quick funding | Startups, entrepreneurs with strong personal credit | Higher rates, personal liability |

| Business Credit Cards | Varies by creditworthiness | 17.49% – 27.49% | Rewards programs, expense tracking | Daily business expenses, building credit | High variable rates, personal guarantee often required |

| Commercial Real Estate Loans | $25,000 – Several million | 5% – 14% (varies by type) | Long terms, property as collateral | Property purchase/refinancing | Large down payments (20-40%), maintenance costs |

| Startup Business Loans | $500 – $5M | 7% – 99% | Less stringent requirements | New businesses, strong personal credit | Higher rates, personal guarantees required |

Conclusion

Choosing the right business loan requires careful consideration of your specific needs, qualifications, and long-term goals. Throughout this guide, we’ve examined twelve distinct financing options available to entrepreneurs in 2025, each serving unique business situations.

Traditional term loans and SBA programs offer lower interest rates but demand stronger qualifications and longer approval timelines. Alternatively, lines of credit and equipment loans provide flexibility for specific operational needs. Business owners facing cash flow challenges might find invoice factoring or financing particularly valuable, though these options typically come with higher costs.

Startups and newer ventures can turn to microloans, personal loans for business, or business credit cards when conventional financing remains out of reach. Companies ready for property investment should explore commercial real estate loans, while those needing immediate capital might consider merchant cash advances despite their higher costs.

Your financial situation, time in business, credit profile, and funding timeline will ultimately determine which option works best. Remember, the lowest interest rate doesn’t always indicate the best choice – factors like repayment flexibility, qualification requirements, and funding speed matter significantly.

Before committing to any business loan, thoroughly review all terms, calculate the total cost including fees, and ensure the repayment structure aligns with your cash flow patterns. The right financing solution should support your growth without creating unmanageable financial strain.

Undoubtedly, business financing continues evolving with economic conditions. Staying informed about current rates and terms will help you secure the most advantageous funding for your enterprise, whether you need working capital, equipment, real estate, or expansion financing.

FAQs

Q1. What are typical interest rates for business loans in 2025? Interest rates vary widely depending on the loan type and lender. Traditional bank term loans generally range from 6.6% to 11.5%, while online lenders may charge between 9% and 75%. SBA loans offer rates between 10.5% and 15.5%. Other options like business credit cards can have rates up to 27.49%.

Q2. What are the requirements for obtaining a $500,000 business loan? Requirements vary by lender, but typically include a strong credit score (often 680+), at least 2 years in business, and annual revenue of $250,000 or more. Lenders will also want to see a solid business plan, financial projections, and may require collateral. Some alternative lenders may have more flexible criteria.

Q3. How do interest rates compare for different types of business financing? Interest rates can vary significantly. For example, term loans from banks may offer rates as low as 6.6%, while merchant cash advances can have effective APRs up to 200%. SBA loans, equipment financing, and business lines of credit typically fall in the middle range, with rates often between 5% and 15%.

Q4. What financing options are available for startups with limited operating history? Startups can explore options like microloans (with rates from 8% to 13%), personal loans for business use (6.5% to 36%), and business credit cards. Some online lenders offer startup-specific loans, though rates may be higher. Crowdfunding and angel investors are non-loan alternatives worth considering.

Q5. How do repayment terms differ among various business loan types? Repayment terms can vary greatly. Term loans typically have fixed monthly payments over 1-5 years. Lines of credit offer flexible repayment on used amounts. Invoice financing ties repayment to customer payments. Merchant cash advances take a percentage of daily sales. SBA loans can extend up to 25 years for real estate purchases.